Exactly How To Secure Yourself From Signing A Negative Mortgage Contract

Article by-Gustafsson EwingWhat sort of information does one need when considering a mortgage? Where can they find the best, most accurate, expert advice? This article has it all for you, from tips to help you engage in the process to tricks to help you get more out of your mortgage, so read on.

Talk to your family and friends about where they got their home mortgages. Sometimes the best recommendations are from those immediately around you. They'll have lots of information on their own experiences with their banks, so you can feel more secure about where you should shop. Really it can save you many hours of time!

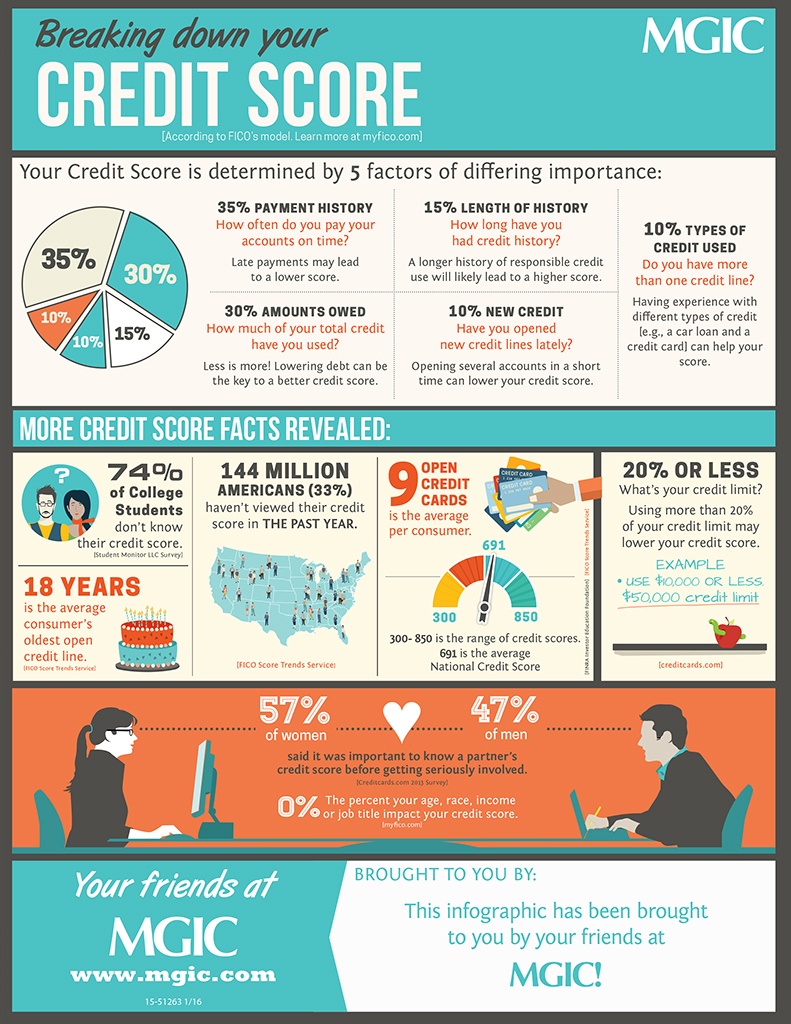

Check your credit report before applying for a mortgage. With today's identity theft problems, there is a slight chance that your identity may have been compromised. By pulling a credit report, you can ensure that all of the information is correct. If you notice items on the credit report that are incorrect, seek assistance from a credit bureau.

Reducing your debt as much as possible will increase your chances of being approved for a mortgage. If you are not in a good financial situation, meet with a debt consolidation professional to get out of debt as quickly as possible. You do not need to have a zero balance on your credit cards to get a mortgage but being deeply in debt is definitely a red flag.

A fixed-interest mortgage loan is almost always the best choice for new homeowners. Although most of your payments during the first few years will be heavily applied to the interest, your mortgage payment will remain the same for the life of the loan. Once you have earned equity, you may be able to refinance your loan at a lower interest rate.

If your appraisal isn't enough, try again. If the one your lender receives is not enough to back your mortgage loan, and you think they're mistaken, you can try another lender. You cannot order another appraisal or pick the appraiser the lender uses, however, you may dispute the first one or go to a different lender. While the appraisal value of the home shouldn't vary drastically too much between different appraisers, it can. If you think the first appraiser is incorrect, try another lender with, hopefully, a better appraiser.

Do not sign a home mortgage contract before you have determined that there is no doubt that you will be able to afford the payments. Just because the bank approves you for a loan does not mean that you could really endure it financially. First do the math so that you know that you will be able to keep the home that you buy.

Don't forget to calculate closing costs when applying for a mortgage, particularly if this is your first time. Above and beyond the down payment, numerous charges exist simply for processing the loan, and many are caught off guard by this. You should anticipate paying up to four percent of the mortgage value in total closing costs.

Make sure that all of your loans and other payments are up to date before you apply for a mortgage. Every delinquency you have is going to impact your credit score, so it is best to pay things off and have a solid payment history before you contact any lenders.

The mortgage loan that is the easiest to get approved for is likely the balloon mortgage. These types of loans are short term and when the loan expires, the mortgage must be refinanced. You run the risk of having the interest rate increase or maybe you won't be in as good of a financial situation as now.

Go online and use a mortgage calculator to find out how much of a loan you can afford. There are many sites that offer these free calculators. Additionally, there are calculators that will tell you the final price you will be paying at the end of the loan and others that show how much you can save by paying extra toward the principal.

If you have filed for bankruptcy, you may have to wait two or three years before you qualify for a mortgage loan. However, you may end up paying higher interest rates. https://www.ft.com/content/9f38f81b-2fe4-4c11-aa47-6d393cd2b6f2 to save money when buying a home after a bankruptcy is to have a large down payment.

Pay off or lower the amount owed on your credit cards before applying for a home mortgage. Although your credit card balances do not have to be zero, you should have no more than 50 percent of the available credit charged on each credit card. This shows lenders that you are a wise credit user.

Pay at least 20% as a down payment to your home. This will keep you from having to pay PMI (provate mortgage insurance) to your lender. If Read the Full Write-up pay less than 20%, you very well may be stuck with this additional payment along with your mortgage. It can add hundreds of dollars to your monthly bill.

Get your credit under control. If you currently have a wallet full of plastic for every occasion, you should downsize. Having too much available credit can harm your loan, even if it is not debt. Close any non-essential accounts. Chose a gas card, a store card, and a single credit card to keep.

Consider a home mortgage plan that incorporates the property taxes into this. Some companies will even give you a break on interest if you do this, as in makes it more likely that you will keep possession of your home. Not paying your taxes could lead to someone else owning the property on which your home resides.

Negotiate a better interest rate on your mortgage by bringing your other assets to the potential lending bank. Transferring your savings accounts, checking accounts and money market accounts to the lenders bank can result in a lower interest rate. A bank may also be more willing to make a loan to a customer of their bank.

Many computers have built in programs that will calculate payments and interest for a loan. Use the program to determine how much total interest your mortgage rate will cost, and also compare the cost for loans with different terms. You may choose a shorter term loan when you realize how much interest you could save.

There are times when the seller of a home will be able to give you a land contract so you can purchase the home. The seller needs to own the home outright, or owe very little on it for this to work. A land contract may need to be paid within a few years.

Hopefully, these tips have taken some of the mystery out of the mortgage process. Maybe now it is time you took the plunge. Use these tips through the process. Now, all you have to do is go shopping for mortgages and remember what you learned here.